One of the most frequently debated topics in retail forex trading is whether a broker operates an A-Book or B-Book execution model.

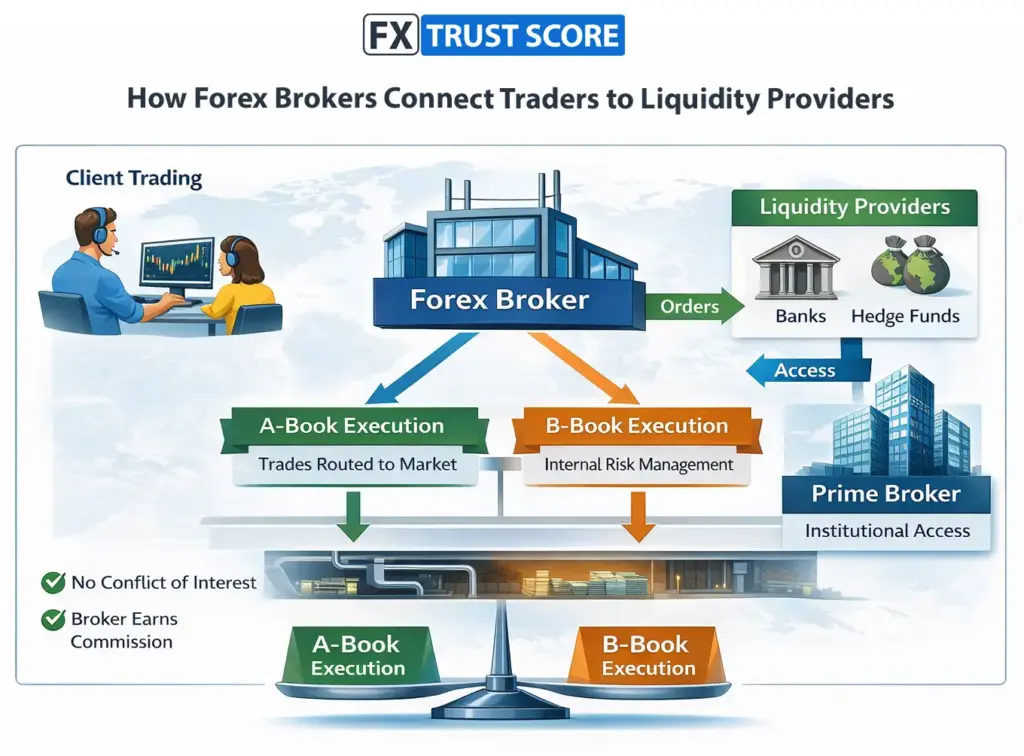

A-Book and B-Book forex brokers refer to different execution models used to handle client trades. In an A-Book model, trades are routed to external liquidity providers such as banks or institutional market makers. In a B-Book model, the broker manages trades internally and may act as the counterparty to the client’s position.

Many traders have heard the terms but are unsure what they actually mean. Some assume that B-Book brokers are automatically dishonest and others believe A-Book brokers always provide better trading conditions. In reality however, the situation is more nuanced.

Understanding how these execution models work can help traders better evaluate broker transparency, execution quality and potential conflicts of interest.

This guide is part of our FXTrustScore Education Series and explains how A-Book and B-Book execution models function in practice and why many brokers use a combination of both.

What Is A-Book Execution?

In an A-Book model, a broker passes client trades directly to external counterparties rather than taking the opposite side of the position.

These counterparties are typically liquidity providers, which may include large banks or institutional trading firms such as:

Citigroup

JP Morgan

XTX Markets

When a trader places an order, the broker routes that order to the market where it is matched with another participant.

In this structure:

the broker does not profit directly from client losses

revenue usually comes from spreads or commissions

trade exposure is transferred to external liquidity providers

Because of this, A-Book execution is sometimes referred to as Straight Through Processing (STP) or agency execution.

What Is B-Book Execution?

In a B-Book model, the broker internally manages client trades rather than sending them to external liquidity providers.

This means the broker effectively becomes the counterparty to the trade.

For example:

if the trader loses money, the broker keeps the loss

if the trader profits, the broker pays the profit

This structure is why B-Book models are often described as market-making.

However, it is important to understand that B-Book execution is not inherently problematic. Many regulated brokers operate market-making models responsibly and provide competitive spreads and fast execution.

Why Many Forex Brokers Use Hybrid Execution Models

In practice, many retail brokers operate a hybrid model that combines both A-Book and B-Book execution. Rather than routing all trades through a single system, brokers may categorise trading activity and manage risk accordingly. For example:

smaller or less consistent trading accounts may be handled internally

large positions may be hedged externally

profitable traders may be routed directly to liquidity providers

This allows brokers to manage risk while maintaining efficient execution.

Why Execution Models Matter for Traders

Understanding broker execution models can help traders interpret differences in trading conditions between brokers. Execution models can influence:

spreads and commissions

order execution speed

slippage behaviour

potential conflicts of interest

However, execution model alone does not determine whether a broker is trustworthy. Regulation, fund protection and operational transparency remain equally important factors.

Regulators such as the Financial Conduct Authority and the Cyprus Securities and Exchange Commission require brokers to maintain fair execution practices regardless of their internal execution model.

How A-Book and B-Book Models Relate to Broker Infrastructure

Execution models form part of the broader infrastructure behind retail forex trading.

As explained in our guide How Forex Brokers Work, brokers sit between retail traders and institutional liquidity providers. They may route trades externally, manage exposure internally, or combine both approaches depending on their risk management framework.

Understanding these mechanics helps traders see beyond marketing labels such as “ECN” or “STP”, which are sometimes used loosely in the retail trading industry.

Why Transparency Matters When Choosing a Broker

For traders, the key issue is not whether a broker uses A-Book or B-Book execution, but whether the broker operates transparently and under credible regulatory oversight.

Well-regulated brokers should:

maintain segregated client funds

disclose execution policies

provide fair pricing and order handling

These factors ultimately play a larger role in broker reliability than the specific execution model used.

Why Understanding Execution Models Is Important

Execution models are one part of the broader infrastructure that supports retail forex trading. Whilst many traders focus primarily on spreads, leverage or trading platforms such as MetaTrader 4 and MetaTrader 5, the underlying execution structure can influence how trades are handled behind the scenes.

Consequently, traders researching brokers should consider not only trading conditions but also how the broker manages trade routing and risk.

Understanding these mechanics can help traders evaluate brokers more effectively and make better-informed decisions when choosing where to trade.

Related Guides

FAQs

An A-Book broker routes client trades directly to external liquidity providers rather than taking the opposite side of the trade.

A B-Book broker manages trades internally and may act as the counterparty to client positions.

Not necessarily. Many regulated brokers operate market-making models responsibly and provide competitive trading conditions.

Yes. Many brokers operate hybrid execution systems where trades may be routed externally or handled internally depending on risk management.

Publication date:

16/03/2026

Author: FX Trust Score

Last updated on March 16, 2026